Changes in tax invoices for 2023: what you need to know

GST (Goods and Service Tax) is a tax charged on most goods and services in New Zealand and is collected by businesses on behalf of the IRD from its consumers. Businesses that are registered for GST are required to issue tax invoices and keep records of their sales and purchases.

However, issuing invoices and recordkeeping can be daunting and time-consuming for businesses – so much so that the IRD has modernised the GST rules to help business owners. These rules have been in effect since the 1st of April 2023.These changes raise important questions for Kiwi business owners, and it’s important to know what they mean for you and your business.

In this article we’re going to cover a number of key changes under the new rules, how they affect purchasing second-hand goods, and how they can be applied to business owners.

What are the new rules?

The requirement for GST invoicing and recordkeeping has been replaced by a more general requirement – providing (and keeping) taxable supply information. The advantage of the new rules gives business owners more flexibility, with the convenience of e-invoicing.

You can save time and money by reducing your admin time (as long as you meet the minimum information requirements set by the IRD!).

We’ve included some key changes you need to know:

New terms changes

- Tax invoices are now known as ‘taxable supply information’

- Debit notes or credit notes are now known as ‘supply correction information’

- Buyer-created tax invoices are now known as ‘buyer-created taxable supply information’

Taxable Supply Information (TSI)

TSI shows what was sold, who sold it, who bought it, and how much GST was charged.

This information can be provided and kept in various ways, such as through accounting software (Xero) or an electronic exchange between your software and your customer’s software (PEPPOL e-invoicing).

These TSI formatting changes are not mandatory as long as the correct information is supplied to the IRD. You can stick with the old rules and receive tax invoices as usual, as the new rules are designed to be less restrictive and more adaptable to different invoicing partners.

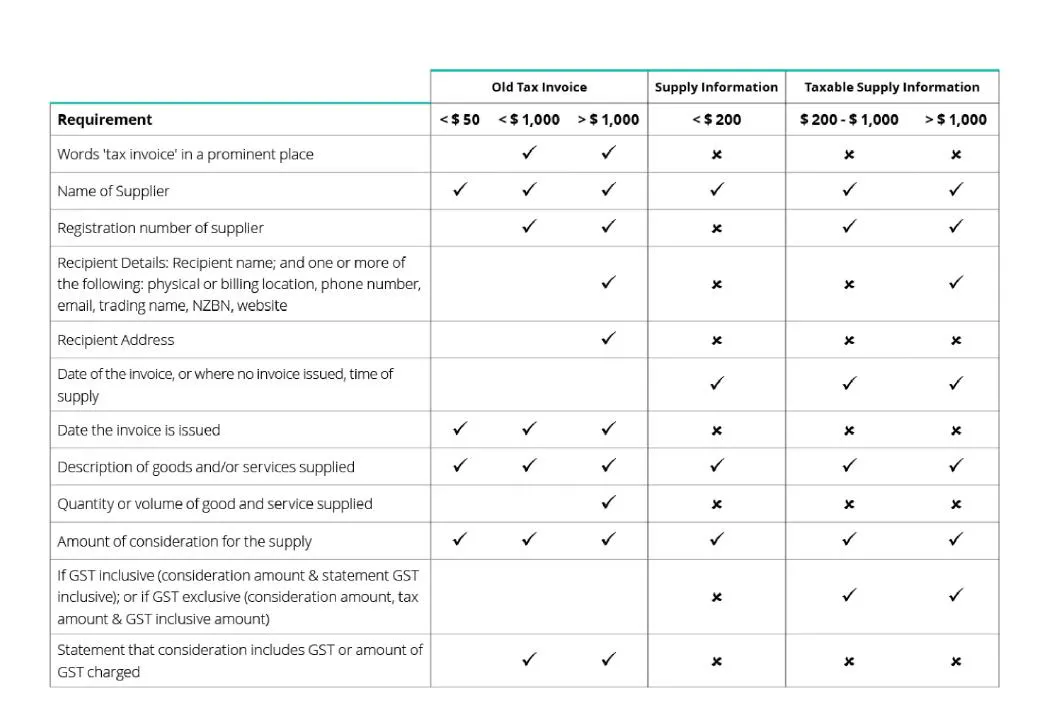

It’s important to note the TSI information required depends on the value of the transaction.For instance, you

don’t need to issue a TSI if the customer is not GST registered, or the GST inclusive amount is under $200 (the low-value threshold has increased from $50 to $200). If the amount is below $200 and you’re using Xero, the information provided within Xero is sufficient.

To learn more check out the IRD’s page on how taxable supply information for GST work.

A quick rundown of these changes is outlined below (source – Deloitte).

How do these changes impact my business?

As a business owner, it’s important to be aware of the changes and understand how they apply to your business. A good starting point is to review your current invoicing and recordkeeping processes and assess whether you need to make any changes or adjustments.

Make sure you keep your customers and suppliers updated on how you will provide and keep taxable supply information. You may need to update your contracts or terms and conditions to reflect these new rules.

Lastly, you may want to take advantage of e-invoicing – it’s a great opportunity to streamline your business operations, receive payments faster and ultimately improve your cash flow. If you’d like to read more on this topic, we have an article on an introduction to e-invoicing for business owners.

Purchasing second-hand goods

To claim GST back on second-hand goods purchased, you need to record the following:

- Seller’s name and trade name

- Seller’s address

- The date on which the goods were supplied

- Description of the goods

- Quantity or volume of the goods

- Total amount payable

Invoices are not normally provided on platforms such as Facebook Marketplace or TradeMe. This can make the invoicing and recordkeeping rules tricky, so be sure to at least gather this information.

Keep in mind GST needs to be managed differently when purchasing second-hand goods from a person or a business that you have an association with. You can learn more about this on our blog: GST on second-hand goods.